Industrial processes currently account for roughly one-quarter of carbon emissions in the United States, with many experts recognizing electrification as an essential step for achieving meaningful decarbonization. Electrifying heating processes at industrial and manufacturing sites, particularly low- and medium‑temperature applications, can directly reduce these industrial emissions. Yet deployment remains stubbornly slow across much of the United States, largely due to a lack of economic viability.

Attribution: Key insight and expertise guiding this piece was provided by Jamie Scripps of Hunterson Consulting.

Solving this economic viability issue requires addressing what’s known as the “spark gap,” which is the difference in cost between electricity and natural gas when each is used to produce heat at industrial sites.

Understanding the structural drivers of this gap is critical to advancing industrial electrification. Also critical is understanding that electricity rate design (i.e., how plays a key role in narrowing the spark gap. While electricity rate design on its own cannot close the spark gap, it is an essential step that can lay the foundation for additional measures and a future with parity in electricity and gas prices.

That parity is a foundational component of making industrial electrification economically viable, which in turn could create conditions allowing for large-scale industrial decarbonization. Reaching that parity first requires stakeholders and policymakers alike to have a clear understanding of what the spark gap is, its effects on industrial electrification, and the opportunities that exist to address it.

So, what exactly is the spark gap?

The spark gap is the difference between the cost of producing heat with electricity and the cost of producing heat with natural gas, adjusted for conversion efficiency (how efficiently an energy source is used to produce heat).

Currently, electricity costs place an outsized burden on industrial sites, making it economically unfeasible for many to move away from natural gas. Understanding how this gap affects industrial sites requires comparing prices on a thermal basis ($/megawatt hour-thermal), meaning how efficiently an energy source can be used to generate heat, not simply on a fuel price basis.

Using the state of Minnesota as an example, let’s look at how this plays out with data from the US Energy Information Administration.

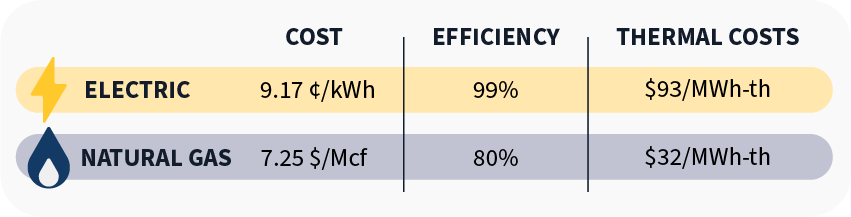

COST COMPARISON OF PRODUCING HEAT WITH ELECTRIC AND GAS ENERGY SOURCES IN MINNESOTA

Sources: “Natural Gas Industrial Price: Minnesota, December 2025,” US Energy Information Administration (US EIA), released March 20, 2026; “Electric Power Monthly: Minnesota, January 2026 YTD,” US EIA, released March 20, 2026. Note: Estimated electricity costs are shown per kilowatt-hour (kWh), estimated gas costs are shown per one thousand cubic feet of gas (Mcf), and thermal costs are shown per megawatt hour-thermal (MWh-th). Efficiency is based on an average electric or gas boiler efficiency.

When converted into thermal costs, that electricity produces heat at roughly $93/megawatt-hour thermal (MWh-th), while natural gas produces heat at roughly $32/MWh‑th. So, even though the electric system is more efficient, the increased efficiency cannot overcome the significant spark gap.

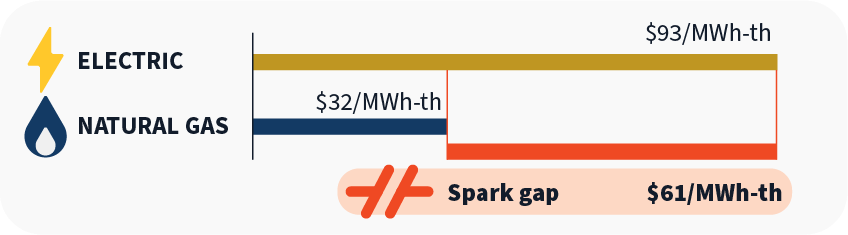

VISUALIZING THE SPARK GAP: THE OVERALL DIFFERENCE IN HEAT PRODUCTION COST USING ELECTRIC VERSUS NATURAL GAS ENERGY SOURCES

Sources: “Natural Gas Industrial Price: Minnesota, December 2025,” US EIA, released March 20, 2026; “Electric Power Monthly: Minnesota, January 2026 YTD,” US Energy Information Administration, released March 20, 2026.

Note: Estimated thermal costs are shown per megawatt hour-thermal.

The resulting spark gap is roughly $61/MWh-th. This differential creates a large and recurring operating cost penalty for industrial sites that switch to electrified systems. And that’s before any upfront capital expenditures are considered.

For perspective, here’s what a spark gap can cost small, medium, and large facilities over the course of a year:

- A small facility (5,000 MWh‑th/year) faces ~$305,000 in annual added cost

- A medium facility (25,000 MWh‑th/year) faces ~$1.5 million

- A large facility (100,000 MWh‑th/year) faces ~$6.1 million

On its own, this massive gap between gas and electricity costs can halt otherwise viable electrification investments, slowing the transition from natural gas and delaying critical industrial decarbonization efforts.

Why the spark gap exists

The spark gap is a product of fundamentally different, and often inequitable, cost structures for both the implementation and usage of electricity and natural gas-powered industrial processes.

Electricity prices generally reflect several variables:

- Generation, transmission, and distribution costs

- Capacity and reliability investments sized for peak demand

- Public policy programs and system obligations

Natural gas prices, by contrast, largely reflect the following:

- Commodity fuel costs

- Pipeline transportation

- Limited recovery of upstream and downstream system impacts

In addition, switching from gas to electricity requires a significant investment in new capital, including necessary but expensive equipment. Electric customers also currently pay for many external costs, especially emissions and climate impacts, through regulatory system rates. This combination of high capital costs and subsequent high operational costs can prove overly burdensome for most companies without adequate rate reform or incentives.

How rate design reform can help

Rate design reform alone cannot fully eliminate the spark gap, but it can play a critically important role. While not a perfect solution, rate design reform can do the following:

- Remove market distortions that penalize electrification

- Ensure customers pay cost‑reflective prices

- Enable flexible electric loads to access low‑cost energy

- Reduce unnecessary exposure to peak‑driven charges

In short, good rate design helps to better ensure that electrification is evaluated on fair economic terms. To strike that fair economic balance, states and public utility commissions could consider implementing reforms, such as those discussed below.

Time‑differentiated energy pricing

Time‑of‑use (TOU), real‑time pricing (RTP), and critical peak pricing (CPP) allow industrial electrified loads to operate during periods of low system cost. When paired with thermal energy storage, industrial facilities can separate electricity consumption from heat demand, dramatically reducing costs while supporting grid reliability.

Coincident peak demand charges

Basing demand charges on system peak periods, rather than a customer’s individual monthly maximum, aligns charges with the true drivers of grid costs. Customers gain the ability to avoid demand charges by operating flexibly, and electrified loads are rewarded for helping the grid rather than penalized for brief internal peaks.

Demand ratchet reform

Shortening ratchet periods, making them seasonal, or tying them to system peaks reduces the long‑term financial risk of a single operational event. This is foundational to making electrification an affordable option for industries.

Electrification‑specific or flexible load tariffs

Dedicated tariffs for electric boilers and industrial heat pumps can do the following:

- Offer lower off‑peak energy prices

- Modify or condition demand charges

- Integrate demand response and dispatchability

These tariffs treat electrified loads as grid assets, not liabilities.

Transitional demand charge protections

Temporary demand charge relief for newly electrified loads recognizes that peak impacts are often short‑lived and decline as operations, storage, and controls mature. These protections reduce first‑mover risk and enable learning on both the customer and utility side.

Leveraging rate design as a key tool for reducing the spark gap

in many cases, with even larger reductions possible under highly flexible operating conditions. Though a meaningful spark gap would still remain and require additional measures to address, leaning into rate design reform and load flexibility provides a strong starting point.

To expand on the progress rate design reform can deliver, states and public utility commissions should consider additional incentives to further shrink the spark gap. Here are examples of potential incentives:

- Offsetting remaining operating cost differences

- Supporting capital investment in electrification and storage

- Reducing risk and accelerating early adoption

These incentives can be intentionally sized and created with the spark gap in mind, targeting what remains after rate design and operational improvements are fully leveraged.

With a mix of effective incentives and well-informed rate designs, several segments of the industrial sector are likely to experience near-term benefits, including the following:

- Low‑ and medium‑temperature processes

- Facilities with operational flexibility

- Sites able to deploy thermal storage

- Regions with relatively lower electricity prices

Industrial electrification is not blocked by a lack of ambition or technology. It is constrained by a pricing system built for a different era that no longer aligns with the current energy landscape. Closing the spark gap requires a foundation of aligned rate design, which can then be built upon with targeted incentives, operational flexibility, and more. All of these components can work in tandem to deliver electrification at fair, cost‑reflective prices, ensuring value for both customers and the grid as a whole.

Keep up to date with all GPI news and posts by signing up for our monthly Better Energy newsletter.