As carbon management projects move from concept to development, one question is becoming increasingly urgent for policy makers, industry leaders, and communities alike: Where can carbon capture and storage be deployed most effectively, and what infrastructure will it require?

Answering this question is essential as reducing emissions at the scale and speed required to meet climate targets will depend not only on expanding clean energy, but also on addressing emissions from existing industrial facilities and power plants. For many sectors, particularly heavy industry, carbon capture and storage (CCS) represents an important pathway to achieve deep emissions reductions while maintaining economic activity and supporting regional jobs.

The decision-making and planning process for deploying CCS requires more than emissions inventories or high-level projections. It requires detailed, facility-level analysis that connects capture opportunities, geologic storage resources, and transportation infrastructure into a realistic picture of how carbon management systems can evolve.

To help meet that need, GPI, working with Carbon Solutions LLC, develops regional deployment scenarios to evaluate carbon capture opportunities at individual facilities, assess available geologic storage, and identify the transportation infrastructure needed to connect them. These scenarios provide a holistic picture of how carbon management systems could be developed regionally.

Carbon management is a system, not a single project

Across all regions studied so far, one conclusion stands out: CCS delivers the greatest impact when it is designed as coordinated infrastructure rather than a collection of isolated projects. Strategic planning of a carbon management system has several benefits:

- Enables shared pipelines and storage hubs

- Lowers costs through economies of scale

- Improves system efficiency

- Creates pathways for additional facilities to participate over time

At its core, carbon management is an infrastructure challenge. It requires answering a complex set of interrelated questions: Which facilities are best suited to capture carbon dioxide (CO2)? Where can it be safely and permanently stored? What pipeline networks are needed to connect them? And how will costs, geography, and policy shape deployment over time?

To date, GPI has modeled three regions representing large portions of the US. The most recent publication, Carbon Capture and Storage Opportunities in the Southeast and Gulf Coast, was released in early 2026. The other two regions analyzed so far are the Mid-Atlantic and the Midcontinent regions.

Using advanced modeling tools and geospatial analysis, GPI evaluated thousands of facilities and storage locations to create cost-optimized regional systems that integrate capture, transport, and storage. The result is not a prediction of exactly what will be built, but a practical roadmap illustrating what is possible under different conditions. The scenarios examine opportunities for carbon capture, transport, and storage infrastructure under different regional conditions, both in the near term and decades into the future.

Key findings across each region

While each region has unique characteristics in the current landscape and future deployment, the overall development trajectory is similar: Early projects connect individual facilities to available storage resources, and over time, those connections expand into larger, shared regional networks. The regional analyses help public and private decision makers understand optimal pathways for deployment and potential barriers that may need to be addressed.

Carbon capture and storage opportunities in the Southeast and Gulf Coast

The Southeast and Gulf Coast region is poised to lead the country in industrial and power-sector innovation through carbon management. Its concentration of industrial and power facilities, access to major ports, extensive geologic storage resources, and evolving policy landscape create uniquely favorable conditions for deployment. The analysis evaluates two scenarios: near-term deployment and midcentury deployment.

Near-term deployment scenario for the Southeast and Gulf Coast

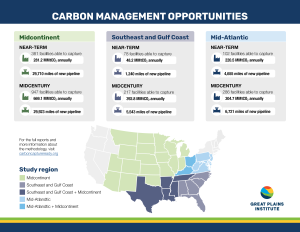

The near-term scenario examines the facilities most prepared to move forward within the next decade, to a decade and a half, either because they have relatively low capture costs or have announced carbon capture projects in development. The analysis identified the following:

- 78 facilities deploying carbon capture

- 48.2 million metric tons of CO2 captured and permanently stored each year

- Approximately 1,300 miles of new CO2 pipeline infrastructure

Early deployment emphasizes smaller pipeline networks that connect one or several facilities to nearby geologic storage hubs. Capture opportunities are concentrated in hydrogen production, natural gas processing and power generation, refining, and other lower-cost industrial sources.

Midcentury deployment scenario for the Southeast and Gulf Coast

The midcentury scenario reflects a more mature carbon management system. In this scenario, capture costs have declined due to experience gained from established projects, and shared pipeline and storage infrastructure is widely available. Under these conditions, deployment expands significantly. The analysis identified the following:

- 217 facilities deploying carbon capture

- 392.8 million metric tons of CO2 captured and permanently stored each year

- Approximately 5,600 miles of CO2 pipeline infrastructure

At this stage, deployment expands across a broader set of industrial and power sectors—including cement, petrochemicals, pulp and paper, and additional generation facilities—and relies on larger, interconnected pipeline networks and shared storage hubs.

Carbon capture and storage opportunities in the Mid-Atlantic

The Mid-Atlantic presents a distinct but equally significant opportunity for carbon management deployment. With a dense concentration of power plants, heavy industry, and access to both onshore and offshore geologic storage resources, the region has the building blocks for large-scale CCS infrastructure. GPI’s 2023 analysis included near-term and midcentury deployment scenarios.

Near-term deployment scenario for the Mid-Atlantic

- 102 facilities deploying carbon capture

- 220.5 million metric tons of CO2 captured and permanently stored each year

- Approximately 4,600 miles of new CO2 pipeline infrastructure

Midcentury deployment scenario for the Mid-Atlantic

- 286 facilities deploying carbon capture

- 304.7 million metric tons of CO2 captured and permanently stored each year

- Approximately 6,700 miles of CO2 pipeline infrastructure

In the Mid-Atlantic, power plants represent the single largest capture opportunity, alongside key industrial sectors such as cement, steel, and refining. The region’s significant geologic storage potential—both onshore and offshore—offers flexibility in how infrastructure networks can evolve.

Carbon capture and storage opportunities in the Midcontinent

The Midcontinent region offers carbon capture opportunities across a range of industries, including many low-cost options in the ethanol sector. It also has significant geologic storage potential, creating opportunities for shared transport and storage infrastructure to serve facilities located far from suitable storage sites. Our 2021 analysis included near-term and midcentury deployment scenarios.

Near-term deployment scenario for the Midcontinent

- 381 facilities deploying carbon capture

- 281.2 million metric tons of CO2 captured and stored annually

- Nearly 30,000 miles of CO2 pipeline infrastructure

Midcentury deployment scenario for the Midcontinent

- 947 facilities deploying carbon capture

- 669.1 million metric tons of CO2 captured and stored annually

- Nearly 30,000 miles of CO2 pipeline infrastructure

Informing decisions in a critical decade

Future outcomes are inherently uncertain. Political landscapes shift, regulatory frameworks evolve, and project-specific considerations vary widely. These scenarios are not a crystal ball. Instead, they are designed to advance informed decision-making by clarifying where deployment is the most promising and what infrastructure will be required to support it.

For policy makers, industry leaders, community organizations, and investors, this analysis provides a clearer understanding of both the scale of opportunity and the deliberate planning needed to realize it.

Explore the full reports:

Carbon Capture and Storage Opportunities in the Southeast and Gulf Coast

Carbon Capture and Storage Opportunities in the Mid-Atlantic

Transport Infrastructure for Carbon Capture and Storage (Midcontinent)