Minnesota has a statutory net-zero emissions target for 2050, which will require emissions reductions in the industrial sector. In 2022, the Minnesota Pollution Control Agency found that gas use in the industrial sector contributed to a greater share of statewide greenhouse gas emissions than gas use in residential, commercial, and electricity generation sectors. Decarbonizing industrial gas end uses is challenging due to high heat needs, specialized equipment, and cost barriers associated with alternative technologies.

To support building a shared understanding about these challenges and potential solutions, GPI has developed a white paper that highlights important regulatory boundaries and jurisdictional considerations for decarbonizing natural gas end uses in Minnesota’s industrial sector.

GPI’s findings on Minnesota gas regulation

Key findings from the paper include the following:

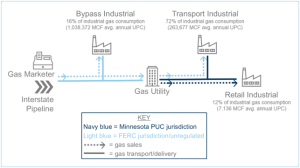

- Most of Minnesota’s industrial gas use comes from transport customers of local distribution companies (LDCs) (72 percent), who purchase gas from third-party suppliers and transportation of that gas from their LDC. The remainder is split fairly evenly between retail customers (12 percent), who purchase both gas and its transportation from their LDC, and bypass customers (16 percent), which are a small number of industrial facilities with exceptionally high per-customer usage that bypass LDC involvement to purchase gas transportation service directly from interstate pipelines.

- Bypass customers purchase transport service that is regulated by the Federal Energy Regulatory Commission (FERC), while customers of gas LDCs are regulated by the Minnesota Public Utilities Commission (MN PUC). Policies that impact LDCs under MN PUC jurisdiction do not encompass bypass usage. Likewise, policies that increase costs for industrial gas users currently under MN PUC jurisdiction may risk incentivizing larger industrial customers to leave the LDC system in favor of cheaper bypass service.

- State policies such as the Energy Conservation and Optimization Act (ECO), Natural Gas Innovation Act (NGIA), and the new gas utility integrated resource planning requirements offer several opportunities for industrial sector decarbonization for customers under MN PUC jurisdiction. However, ECO and NGIA include significant exemptions for large LDC customers that can demonstrate competitive economic pressures or the potential to bypass LDC infrastructure—limiting the scope of these laws for the industrial sector in particular.

Figure 1. Industrial gas customers in Minnesota by jurisdiction and usage

Sources: “Natural Gas Data Sources,” EIA; “Annual Report of Volumes, Revenues, and Customers by Company (1997–2023),” American Gas Association. Note: This data is collected through EIA Form 176, a mandatory survey of all companies that deliver natural gas to consumers or that transport gas across state lines. Usage values are for 2022 usage and were collected in 2023.

Advancing industrial decarbonization in Minnesota

Understanding these jurisdictional boundaries is critical for developing effective industrial decarbonization strategies. As Minnesota works toward its 2050 net-zero goal, frameworks must consider jurisdictional borders as well as economic and operational considerations for industrial customers.

This paper provides a foundation for those conversations by explaining the complex landscape of industrial gas regulation in Minnesota.

The full white paper is available to everyone on our website. If you’d like to discuss any questions or information presented in the paper, please contact our Energy Systems team.